Bitcoin Isn’t a Bet. It’s the US Government’s Backup Plan.

How BlackRock, Strategy, and Two New Laws Are Building the Next Dollar

The news of Jensen Huang flying to Anchorage, Alaska, to board Air Force One caused me to stop and re-read it genuinely. Not because a Nvidia CEO wanting access to China’s market is surprising. But because of how it happened. Trump called him personally. Huang flew to Alaska. He got on the presidential plane.

That is not a courtesy. That is a statement.

On May 12, Trump landed in Beijing for a four-day summit that looked less like a diplomatic visit and more like a Davos off-site with Air Force One branding.

Larry Fink of BlackRock.

Tim Cook of Apple.

Elon Musk, representing both Tesla and SpaceX.

Kelly Ortberg from Boeing. And Jensen Huang, the CEO of the company whose GPU architecture is the one resource China cannot replicate at scale yet, was confirmed as a last-minute addition after Trump called him.

To understand why that detail matters, you need to understand what this meeting was actually about. And it was not primarily about trade tariffs.

The Hormuz Variable

The Strait of Hormuz has been effectively closed since February 28, when the US and Israel launched strikes on Iran. Roughly 20% of the world’s oil transits through that narrow chokepoint, and since Iran’s retaliation sealed it, energy markets and global shipping have been rerouted around the crisis.

China has been publicly pushing Tehran to return to the negotiating table. Whether that represents a concern for regional stability or calculated leverage over both Washington and Tehran is a question worth sitting with.

Probably both.

Because that is the context in which Trump arrived in Beijing.

Not from a position of unchallenged dominance.

From a position where he needs something from China, and Beijing knows it. The Hormuz crisis, more than tariffs, is what put Trump on that plane.

The Dollar’s Structural Problem Nobody Wants to Say Out Loud

Let me say something plainly that most financial media dances around: the US dollar has a structural problem with no painless exit.

The Triffin Dilemma describes it precisely. When one nation’s currency becomes the global reserve currency, that country must run persistent trade deficits to supply the world with the liquidity it needs. Over decades, those deficits corrode the very foundation of the currency’s credibility. The 2008 financial crisis confirmed this for Asia, and the lesson landed hardest in Beijing.

Trump himself acknowledged as much, stating that a weaker dollar would benefit American exports. That is a president signaling, in public, that the current dollar trajectory is unsustainable long-term. Jacques Rueff, a French economist, eloquently stated decades ago that the exchange rate serves as the mechanism for flushing out a currency’s accumulated policy errors.

China drew its conclusions around 2000. Since then, Beijing has accumulated gold at a scale that is difficult to fully audit, because large volumes of gold enter China and very little comes back out. By pricing oil and gold in yuan, Shanghai has now established an indirect convertibility between the renminbi and hard assets.

Economist Charles Gave of Gavekal Research has tracked the resulting monetary convergence across Asia since 2018 and argues that the renminbi has entered the second phase of its rise against the euro.

China’s current account surplus exploded in 2025, reaching a record $735 billion, up from $424 billion in 2024. The manufacturing surplus, measured by Chinese customs, exceeded $2 trillion for the year. Those are not numbers that leave Washington indifferent.

Hong Kong’s Shadow Dollar Machine

Here is where it gets genuinely alarming for the Federal Reserve.

During the Cold War, European banks accumulated dollar deposits outside the US jurisdiction and began issuing dollar-denominated loans using those deposits as reserves, bypassing the Fed entirely. This became the “Eurodollar” system: a parallel dollar supply that grew beyond anyone’s initial design and circulates to this day outside American monetary control.

Brad Setser, a former US Treasury advisor, estimates that Chinese government-linked institutions hold roughly $6 trillion in foreign assets, with approximately $3 trillion sitting in shadow reserves inside state banks and policy banks, and routed through Hong Kong rather than appearing in official People’s Bank of China accounts. The Bank for International Settlements has also noted this dynamic.

Apply even a conservative banking multiplier of 10 to those $3 trillion in shadow reserves, and you’re looking at a theoretical $30 trillion in dollar-denominated credit capacity operating outside Fed oversight. For context, the US M2 money supply reached $22.6 trillion in early 2026, a historical record.

This creates two deeply uncomfortable scenarios for Washington. Dollars created through Hong Kong do not flow back to finance American deficits. They circulate inside a Chinese-managed global supply network. And in a crisis involving Hong Kong-issued dollars, those banks cannot access the Fed’s lending window because they created those dollars without permission. The resulting credit crunch could be spectacular.

You now understand why Trump brought both Musk and Huang to Beijing.

China is gaining access to coveted space technology through SpaceX. Nvidia chips give China access to the AI compute it needs even more. These are real currencies of negotiation, not photo opportunities.

Bitcoin as the American Backup

Now we get to the part that most European analysts still treat as fringe: the idea that Bitcoin is the United States’ contingency hedge against a dollar transition.

I tracked every phase of what became known as Operation Chokepoint 2.0, having worked through that period with Data Factory. The systematic debanking of crypto companies under the Biden administration was documented in a 51-page report published by the House Financial Services Committee in December 2025, confirming that at least 30 digital asset entities had been cut off from the banking system between 2022 and 2024 through regulatory pressure on 24 banks.

Then came January 11, 2024: BlackRock launched its Bitcoin ETF. When the world’s largest asset manager launches a product of that nature, you do not do it without White House awareness. That was a policy shift dressed in financial product packaging.

Since then, the GENIUS Act establishing the first federal framework for payment stablecoins was signed by Trump on July 18, 2025. Last week, on May 14, the Clarity Act cleared the Senate Banking Committee 15–9, setting up the jurisdictional boundary between the SEC and CFTC on all digital assets. The White House wants the bill signed by July 4, framed as a 250th anniversary gift to the country.

No law currently authorizes a Bitcoin-backed stablecoin. But these two pieces of legislation build the regulatory architecture that allows corporate balance sheets to hold Bitcoin legitimately, and that clears the path for banks to integrate digital assets into their operations. Strategy, the company formerly known as MicroStrategy, is already knocking on the doors of JP Morgan and its peers.

The math underneath all of this is straightforward. Through BlackRock and Strategy alone, the United States holds more institutional Bitcoin than any other country on earth. If Bitcoin becomes the collateral layer of a new monetary regime, America arrives at that future already positioned. Is this guaranteed? Of course not. But it is not fringe thinking. There is a serious policy logic running underneath it, and it doesn’t require anyone to say it out loud.

When the Economy Grows, and Jobs Disappear

The final dimension of this summit that deserves more attention is the one that disrupts the standard US-China competition narrative.

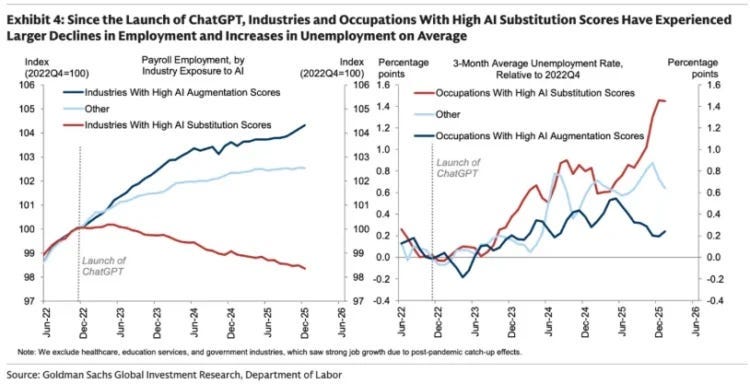

Goldman Sachs published data in April 2026 showing AI is now eliminating roughly 16,000 net jobs per month in the United States. The substitution effect is destroying around 25,000 positions monthly; the complementarity effect is creating about 9,000 new ones. Young adults, Gen Z, are disproportionately affected, especially in the junior, entry-level white-collar jobs they were educated for.

Here is the uncomfortable part:

This is happening while the economy is growing. US Q3 2025 GDP came in at 4.4% annualized, the strongest in two years. Q1 2026 bounced back to 2.0%, with business investment surging 10.4%, the fastest pace in roughly three years, driven almost entirely by AI infrastructure.

The economy we’re seeing unfold now is characterized by growth in GDP coupled with a decrease in employment. That has never happened before at this scale. The social contract that economic growth distributes wealth through employment is about to crack.

And yes, genuinely worrying.

Employment is the mechanism by which productivity gains reach the population. Without it, growth becomes increasingly theoretical for most people.

For the US-China competition, however, this creates a counterintuitive advantage for Washington. China’s strategic moat has always been its labor force. China graduates between 1.3 and 1.5 million engineers per year, against roughly 130,000 in the United States, a 10-to-1 ratio that does not shrink quickly. But if AI and robotics increasingly replicate human labor output at scale, the numerical weight of 1.4 billion workers counts for less than a competitive differentiator. The balance shifts toward who controls the technology stack.

Which is precisely why Jensen Huang’s boarding Air Force One in Alaska was the most important moment of the entire trip. The most valuable thing Trump brought to Beijing was not a trade offer or a diplomatic gesture. It was access to the most powerful AI hardware, held by a company the president could invite or uninvite from the plane with a phone call.

That, and the Taiwan question?

Trump confirmed he discussed arms sales to Taiwan “in great detail” with Xi Jinping, marking a quiet but significant break from the Six Assurances doctrine that has governed US policy on this issue since 1982. Whether that is transactional pragmatism or genuine strategic erosion is a question no one can answer cleanly yet.

What I can say is this:

When a sitting US president negotiates the terms of a sovereign ally’s defense with the ally’s primary adversary, the world has shifted in a way that does not easily shift back.

The technology window for dominance appears to be around 10 years or fewer, given how cycles have compressed:

The transistor arrived after World War II, the internet came 50 years later, and AI arrived 20 years after that. Whoever holds the computational advantage at the start of that window may well hold it at the end. And for the first time in this race, nobody can be certain who that is.

Thanks for reading. Excited to read your comments. I’m still not sure if what happened in Beijing was a masterstroke or a slow-motion mistake. But I don’t think anyone is.